LAWYER FINANCIAL PLANNING & WEALTH CREATION

Table of Contents

Introduction:

₹1 crore lawyer earning ₹30% tax leakage through ignorance loses ₹30 lakhs yearly. Proper structuring converts ₹1.2 crores take-home to ₹2 crores investible surplus. Lawyers practicing tax law ignore personal taxation—ironic self-sabotage costing ₹5-10 crores by age 50. Real estate timing adds ₹2-3 crores alpha; equity SIPs compound ₹50 lakhs to ₹5 crores (15 years @15% CAGR).

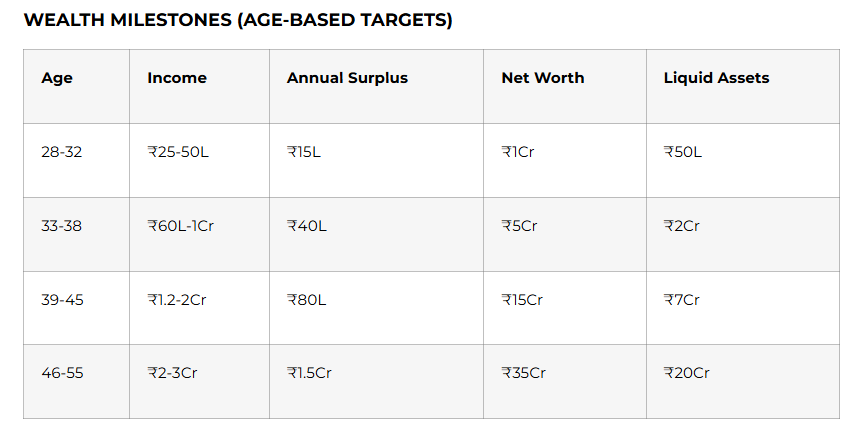

India’s legal wealth creation follows three phases: Years 1-5 (survival → ₹50 lakhs liquid), Years 6-15 (accumulation → ₹5 crores net worth), Years 16+ (compounding → ₹25+ crores legacy). Asset protection shields ₹10 crore practices from matrimonial disputes, professional indemnity claims. Succession planning ensures ₹20 crore firms survive generational transition.

Financial mastery multiplies legal earnings 5x through tax alpha (20% savings), investment alpha (8% outperformance), asset protection (zero losses). If ₹50 lakhs annual surplus seeks ₹10 crore retirement corpus, tax leakage stresses, practice valuation motivates legacy, systematic wealth creation delivers financial independence by age 45.

TAX OPTIMIZATION FRAMEWORK (20% SAVINGS)

Income Structuring (₹25L → ₹40L Take-Home)

text

Practice Income: ₹1Cr (professional fees)

– Section 44ADA: 50% presumption (₹50L taxable)

– Expenses: ₹25L (office, travel, software)

Taxable: ₹75L @25% = ₹18.75L tax

Restructured:

Practice: ₹60L (44ADA → ₹30L taxable)

Consulting LLP: ₹40L (salary ₹20L, profit ₹20L)

Total Tax: ₹12L (₹6.75L saved)

Business Expense Maximization

text

Eligible (100% deductible):

– Office rent (metro limits)

– Law books/journals subscription

– Conference fees (FICCI, Bar Council)

– Laptop/software (₹2L annual)

– Travel (50% client meetings)

Section 80C/80D Max-Out:

text

80C: ₹1.5L (PPF, ELSS, tuition)

80D: ₹25K health insurance

80G: 50% donations (PM CARES)

NPS 80CCD(1B): ₹50K additional

INVESTMENT ALLOCATION (15% CAGR TARGET)

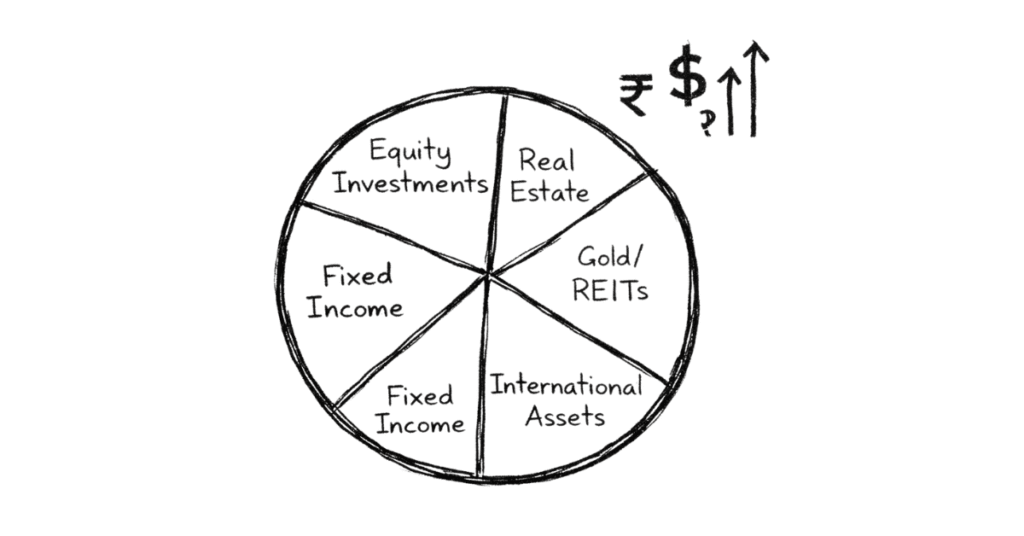

Core Portfolio (₹50L Annual Surplus)

text

40% Equity SIPs: ₹20L (Nifty 50, Smallcap)

25% Real Estate: ₹12.5L (under-construction premium)

20% Gold/REITs: ₹10L (inflation hedge)

10% Fixed Income: ₹5L (FD, Bonds)

5% International: ₹2.5L (US Tech, Nasdaq)

15-Year Compounding:

text

₹50L/year × 15 yrs @15% = ₹24.5Cr corpus

Market Return: 12% = ₹17.2Cr

Alpha: 3% = ₹7.3Cr difference

Real Estate Timing Matrix

text

2025-27: Under-construction (20% alpha)

2028-30: Ready possession (10% rental yield)

2031-35: Redevelopment plays (30% alpha)

Avoid: Ready luxury (0% alpha)

ASSET PROTECTION STRUCTURES

Practice Continuity (Zero Downtime)

text

LLP Structure: Practice + assets ring-fenced

Succession: 51% equity to spouse/children

Keyman Insurance: ₹5Cr coverage (premium ₹5L)

Non-Compete: 3 years post-exit

Matrimonial Shielding

text

Pre-Nuptial: Practice valuation excluded

HUF Structure: Ancestral + self-acquired separation

Gift Deeds: Assets to parents (pre-marriage)

LLP Profit: Not personal income

Indemnity Coverage:

text

Professional Liability: ₹5Cr (₹3L premium)

Cyber Insurance: Client data breach (₹1L premium)

Directors Liability: Advisory roles (₹2L premium)

INVESTMENT OPPORTUNITIES

Equity Picks (20%+ CAGR Potential)

text

Legal Tech: SpotDraft, MyAdvo (early stage)

Litigation Funding: Anand Rathi, Karvy

Alternative Assets: Art, Wine (15% IRR)

Real Estate Alpha

text

Bengaluru Whitefield: 25% 3-year alpha

Pune Hinjewadi: 20% IT corridor

MMR Redevelopment: 35% premium (Dahisar)

NRI Dollar Assets:

text

US REITs: 8% yield + 3% appreciation

Nasdaq ETFs: 15% CAGR (tech focus)

Singapore Property: S$1M (rental yield 4%)

CASHFLOW MANAGEMENT SYSTEM

Monthly Allocation (₹1Cr Annual Income)

text

50% Investments: ₹41.7L

30% Lifestyle: ₹25L (housing, school, car)

15% Reinvest Practice: ₹12.5L (hiring, marketing)

5% Emergency: ₹4.2L (6 months expenses)

Liquidity Ladder:

text

48 Hours: ₹50L (savings account)

30 Days: ₹2Cr (liquid funds)

90 Days: ₹5Cr (debt mutuals)

6 Months: Property (rental income)

SUCCESSION & LEGACY PLANNING

Practice Valuation (3X Profit Multiple)

text

₹1Cr monthly profit × 12 = ₹12Cr

3X multiple = ₹36Cr enterprise value

Client book: ₹18Cr (2X recurring revenue)

Team/systems: ₹12Cr (replacement cost)

Goodwill: ₹6Cr (brand/practice area)

Transition Framework:

text

Phase 1: Junior partner induction (20% equity)

Phase 2: Profit sharing (50:50 split)

Phase 3: Full handover (₹20Cr payout)

Will & Trust Structure

text

Testamentary Trust: Minor children protection

Family Settlement: HUF asset distribution

Practice LLP: Continuity clause

Charitable Trust: 10% wealth legacy

DAILY FINANCIAL RHYTHM (30 Mins/Day)

Practice Owner (₹1Cr/Month Revenue)

text

8 AM: 5-min P&L dashboard (realization rate)

10 AM: Client payment follow-up (₹5L pending)

3 PM: Investment SIP review (₹5L auto-debit)

6 PM: Tax calendar check (TDS, GST returns)

Sunday: Portfolio rebalance (30 mins)

Weekly KPIs:

text

Collections: 95% of billed

Realization: 92% target

Junior Revenue: ₹10L generated

Tax Paid: Quarterly advance complete

TAX CALENDAR & DEADLINES

text

Apr 15: TAN registration (practice)

Jun 30: FY 24-25 TDS returns

Sep 15: Advance tax Q2

Oct 31: GST annual return

Jul 31: ITR filing (AY 25-26)

Quarterly Advance Tax:

text

Q1 (Jun): 15% annual liability

Q2 (Sep): 45% cumulative

Q3 (Dec): 75% cumulative

Q4 (Mar): 100% cumulative

Interest: 1% per month (section 234B/C)

CASE STUDY: ₹28Cr NET WORTH @ AGE 42

text

Profile: RERA lawyer, 15 yrs practice

Peak Revenue: ₹2.4Cr (2024)

Tax Strategy: LLP + expenses = 18% effective tax

Investments: 60/30/10 (equity/RE/gold)

Real Estate: 4 properties (₹12Cr value)

Practice Value: ₹8Cr (recently sold)

Liquid: ₹8Cr (US REITs + equity)

Annual Passive: ₹1.2Cr (4% withdrawal)

Key Decisions:

text

2018: Whitefield flat (3X appreciation)

2020: Smallcap SIPs (25% CAGR)

2022: LLP restructuring (₹40L tax saved)

2024: Practice sale (₹8Cr cash)

IS FINANCIAL MASTERY YOUR DESTINY?

Master Wealth If:

text

✓ Numbers energize (ROI calculation)

✓ Long-term compounding motivates

✓ Tax optimization excites

✓ Asset protection paranoia

✓ Legacy > lifestyle preference

Delegate If:

text

✗ Finance bores/overwhelms

✗ Lifestyle > wealth priority

✗ Trust family office/CA

✗ Early retirement target

Ultimate Payoff: Age 50 comparison

text

Tax-Ignorant Lawyer: ₹3Cr net worth, 35% tax, stress

Financial Master: ₹28Cr corpus, ₹1.2Cr passive, choice

Difference: Generational wealth vs paycheck dependence

Legal earnings without financial systems = sandcastles. Tax optimization + investment alpha + asset protection = empires.